yield curve based on yield curve

It occured to me the other day that based on certain models of the yield curve, it should make predictions about itself. It would be interesting to know how often it has been correct though.

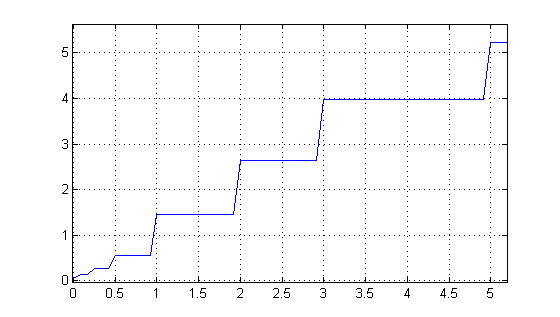

As a start, we can convert the daily yield curve into implied short-term rates in the future. For instance, using the treasury yields as published here yesterday, we get these implied average rates over certain durations:

It says that the short-term rates will rise at about 1% per year and in five years it will stabilize at around 5%. Here is a close up at the short end.

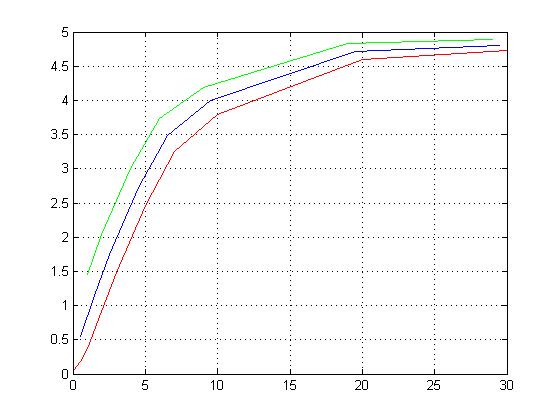

And these translate into the following “standard” yield curves at 6 months (blue) and 1 year (green) from now, compared to currently (red).

There is no guarantee that this will be correct (that is something that needs to be checked against past data), but I distinctly recall that within the past two years the yield curves have, as a rule, been overly optimistic (too steep) on the short end.