2014/04/7

latency arbitrage

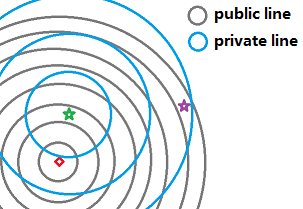

Michael Lewis has been in the news for his new book, Flash Boys, decrying the problems brought about by a system ill equipped to deal with high frequency trading. The core problem can be stylistically summarized by this picture:

Michael Lewis has been in the news for his new book, Flash Boys, decrying the problems brought about by a system ill equipped to deal with high frequency trading. The core problem can be stylistically summarized by this picture:

I place an order from the location of the red square to the green and purple exchanges on which trades occur. My communication capability on the gray “public” channel is slower than the communication capability of some competing agent on the blue “private” channel. Therefore, triangle inequality notwithstanding, the competing agent observes my actions at the green exchange and reacts at the purple exchange before my order arrives there. It appears to me exactly like I have been scooped by somebody acting anti-causally, so what happened?

(Read the article)

Comments(1)

Comments(1)